SecureMyData

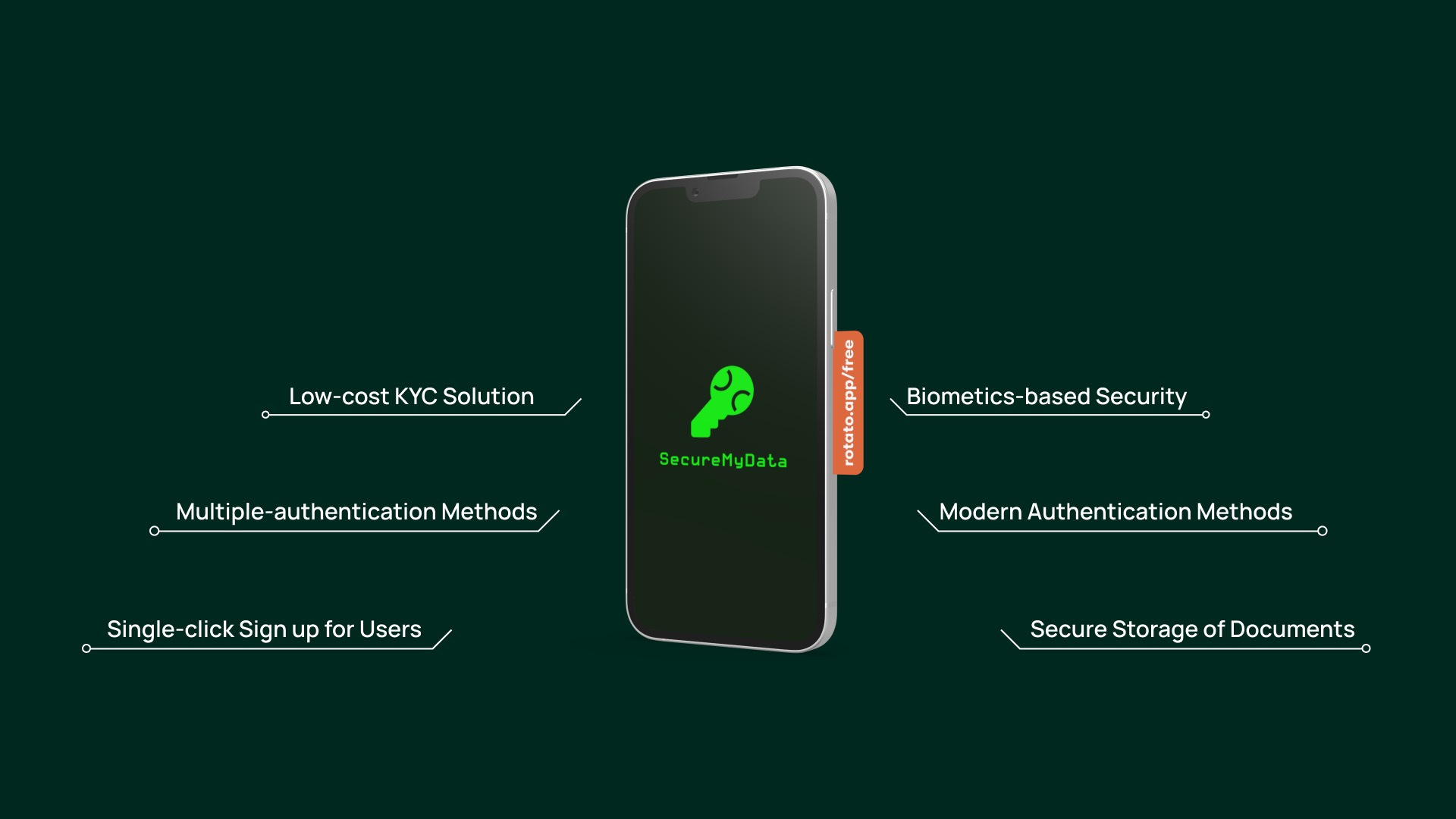

SecureMyData is a blockchain-based solution for securely storing your IDs and documents and securely sharing them with institutions. The product aims to shorten the KYC time for the Average Joe and bring down the KYC (abbreviation: Know Your Customer) costs for institutions. The idea is that a user signs up for SecureMyData, shares their IDs, documents, and financials, and with a "single-click" sign-up button is able to sign up for any service or product. This could range from signing up for a crypto exchanges, insurances, betting services, brokerages, credit services, travel visas, certifications, etc. With a single-click, the user can share their documents and based on relevant regulations, will be asked to fill out outstanding forms and the user can later track which services have access to their data and when this data was shared. The blockhain private key remains with the user and they have the ultimate control to share their public keys. This project was made during the Product Studio program at Cornell Tech with JPMorgan company advisors and stakeholders.

Market Research

During our market research, we targeted retail bank managers, banking professionals, IT experts, and average customers. All were interviewed by team members in which we asked them about their banking experiences, from a consumer point of view and from an industry point of view. From both sides, the main problem that was identified was that the current onboarding process takes a lot of time for both the customers and bankers. A faster KYC process will allow for customers to easily sign up for that service and also enable bankers to quickly onboard their clients and scale up. Another point that was constantly brought up was that financial and KYC fraud happens a lot and sometimes a strenous KYC process is required to address those issues. Incumbents in this sector include Plaid, CLEAR, Onfido, and Okta, that often provide KYC and verification services.

Quick Facts

Between October 2020 and October 2021, the average ID fraud rate was 5.9%, compared to an average rate of 4.1% in 2019.

Global E-KYC Market Predicted to Garner $1.37 Billion by 2028, Growing at Healthy CAGR of 21.5%.

In the UK alone, an estimated 25% of customer applications are abandoned due to KYC friction.

Consumers reported 2,878,566 incidents of non-identity theft fraud in 2021, which resulted in more than $6.1 billion in financial losses, with a median loss of $500 per incident.

Identity theft complaints topped the list of fraud reports the FTC received in 2021, with 1,434,695 complaints.

The average document fraud rate for 2021 was 5.9%, compared to 1.53% for selfies and 0.17% for videos. Far fewer fraudsters trying to attack biometric check compared to documents.

Ideation

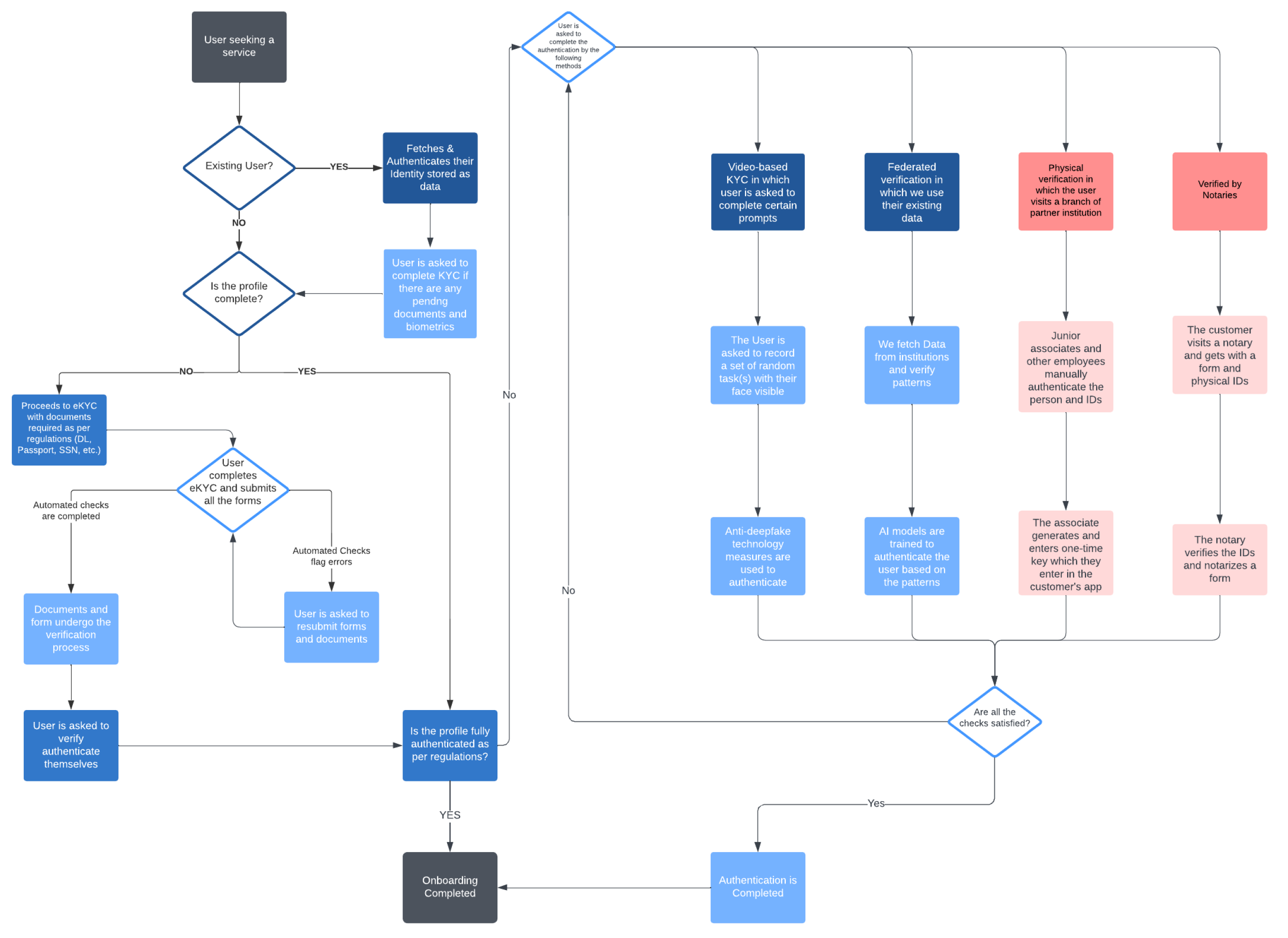

Based on our research, we decided to address the problems of a long KYC process and the security issues. During our brainstorming sessions, we came up with approximately 100 different possible solutions and used a "funnelling" method to filter out the feasible options. Our final idea was a decentralized blockchain-based KYC solution that securely stores the IDs and documents of a user, gives them the ability to share their data, enables them to use a them access to a secure "single-click" sign-up solution, and gives them the ability to track their own data. From an institution's perspective, the idea is to create a framework that allows them to incorporate the "single-click" sign-up solution with their existing KYC solutions, improve the security of data transmission, decrease the KYC cost, and update IDs easily. Below is a user flow chart that explains the process for both users and institutions. The digital framework also accounts for physical verifications in-case of any failures or errors.

Top Risks

Based on our evaluations we identifies top three risks that affects our product. These are as follows:

- Although this may seem to be a niche market, there are many players as per our industry research. The adoption of our product depends upon the ease of onboarding and seamless customer experience.

- Getting organizations and customers to trust the product is difficult due to security, privacy, andtrust issues which makes the sales cycle longer.

- Most incumbent banks and financial institutions use their own KYC processes. Low adoption from companies might result in low adoption from users.

Experimentation

To evaluate our risks and the feasibility of our product, we decided to conduct three different experiments to analyse them. These experiments were tested on individuals based in the United States from 21 to 65 years old. Figma prototypes were made for different experiments and tested on individuals. Their actions were recorded by the team members and they were also quizzed about their overall experience and certain decisions. Two experiments validated our ideas whereas the third experiment gave us an inconclusive result due to lack of data from different sectors. These experiments, prototypes, and the overall product pitch can be viewed in the deck below.

This idea was made possible with help of my Cornell Tech teammates, Alexa Muratyan, Pallavi Bansal, Parren Chen, and Stratos Botis. We were randomly placed together but were perfectly as a team. Overall deliverables of this project include Market Research, User Interviews, Ideation, De-risking, Value Creation Analysis, Market Strategy, Business Decks, Experimentation, Results Analysis, Low-fidelity prototypes, and Project Roadmap.